Aave’s risk management provider LlamaRisk has published a formal incident report mapping two scenarios for how the bad debt created by the Kelp DAO bridge exploit could crystallise across the protocol’s markets. The report was co-authored alongside other Aave service providers and posted to the governance forum on April 20. The final outcome hinges on a single decision Kelp DAO has not yet made public, and both paths carry significant costs for the thousands of depositors still waiting to access their locked funds.

What the two scenarios mean for Aave’s markets

The report centres on how Kelp DAO chooses to allocate the losses from its drained bridge adapter. Under Scenario 1, the roughly 112,204 unbacked rsETH tokens are treated as a loss shared equally by all rsETH holders across every chain. That would impose a 15.12% haircut on every token in existence, producing an estimated $123.7 million in bad debt for Aave spread across seven markets on five networks. Ethereum Core would absorb the largest absolute share at $91.8 million, though its deep WETH reserve means the shortfall represents just 1.54% of the pool. Mantle takes the proportionally harder hit at 9.54%. LlamaRisk noted that Aave’s Umbrella WETH module, currently holding approximately $54 million in staked aWETH, could partially offset the Ethereum Core deficit under this path.

Scenario 2 considers the exploit as an L2-only issue. The rsETH on the Ethereum mainnet, backed by Kelp’s actual staking deposits and unaffected by the bridge adapter, would be worth its full value. Layer 2 rsETH, however, would be repriced to reflect the adapter’s current backing ratio of just 26.46%. That means a 73.54% haircut on all remote-chain rsETH collateral, pushing the total bad debt estimate to $230.1 million. Mantle faces a 71.45% WETH shortfall, Arbitrum 26.67%, and Base 23.28%. Ethereum Core escapes unharmed. Each scenario distributes pain very differently, spreading it thinly across all chains in the first case, or concentrating it entirely on L2 depositors in the second.

The treasury backstop and private bailout talks

LlamaRisk confirmed that the Aave DAO treasury holds $181 million in assets as of April 20, including $62 million in Ethereum-correlated holdings, $54 million in AAVE tokens, and $52 million in stablecoins. Service providers have already secured indicative commitments from several ecosystem participants toward covering a potential shortfall, though no figures have been disclosed. Separately, sources cited by Cryptopolitan on April 21 said Aave and Kelp are currently negotiating a potential bailout independent of LayerZero, with the best-case target being roughly 110,000 ETH to fill the gap.

Kelp and LayerZero trade blame as pressure mounts

While Aave works through its exposure, a public dispute has erupted between Kelp DAO and LayerZero over who bears responsibility for the configuration failure. LayerZero stated that Kelp chose a single-verifier setup against its recommendations. Kelp pushed back, arguing that LayerZero’s default GitHub configuration and documentation promote the same 1-of-1 DVN setup and that approximately 40% of protocols on LayerZero use that exact configuration. In response, LayerZero announced it will stop signing messages for any application still running a single-verifier setup, forcing a mandatory migration across its ecosystem. Security researchers have separately flagged the attack pattern as closely matching the operational signature of North Korea’s Lazarus Group.

Stablecoin markets and the $300M secondary crunch

The damage has extended well beyond the rsETH pools. In the 24 hours after the exploit, whales including TRON founder Justin Sun and exchange MEXC pulled billions from Aave, pushing ETH, USDT, and USDC pools to 100% utilisation. With no idle liquidity left, depositors could not withdraw their funds. Trapped users responded by borrowing approximately $300 million against their own locked stablecoin positions at steep cost, a secondary crunch that monetsupply.eth, head of strategy at Spark, described on X as a direct consequence of the original freeze spreading into unrelated markets.

AAVE price stages a partial recovery

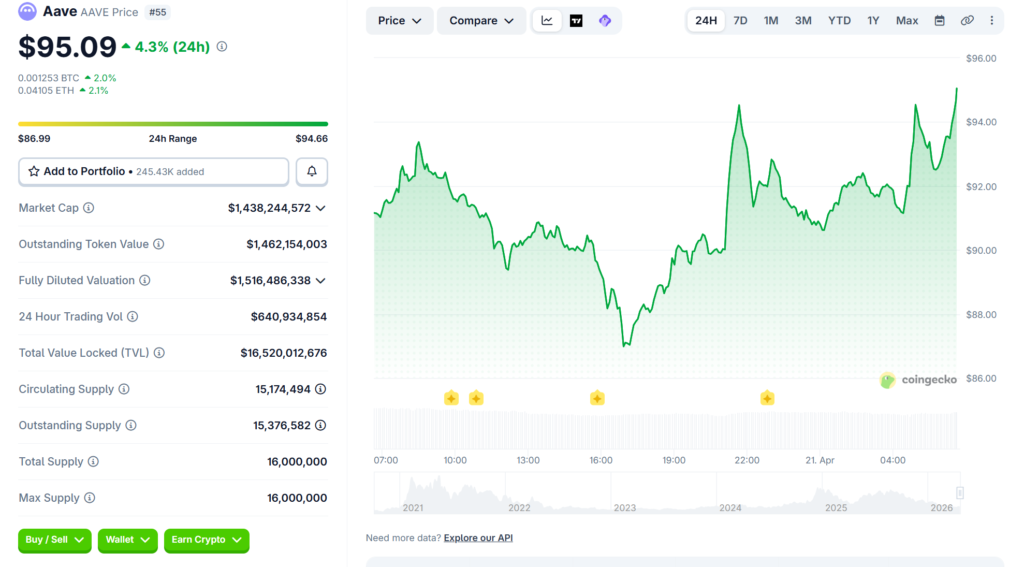

AAVE is trading at $95.09 on April 21, up 4.31% in the past 24 hours, with a trading volume of $640.9 million. The token had fallen 17% from $111 to $92 immediately after the April 18 exploit. The seven-day picture remains negative at -5.25%, and with a circulating supply of 15 million AAVE, the protocol’s market capitalisation stands at approximately $1.44 billion.

The modest recovery reflects cautious optimism around the treasury backstop and the emerging bailout negotiations, though analysts warn that the AAVE price will ultimately be determined by the final bad debt figure, a number that depends entirely on the decision Kelp DAO has yet to announce.